What Kills the Memory Trade?

It's not enough to call it a bubble!

The financial press is torn between calling the rally in memory stocks a bubble or the start of a new paradigm. Some say a parabolic rise in share price is itself enough to reduce your allocation, regardless of fundamentals, because nothing keeps going up and to the right indefinitely. Others highlight years of supply being secured, a lack of a serious alternative to the Memory Three, and long-term agreements supporting the eventual re-rating of the memory industry as non-cyclical.

The stock market is a weighing machine. The value of a public company is the range of future outcomes weighed by the probabilities of each, using all available information at any given time. Whether you hold multiple outcomes in mind is a you problem; the market does it by virtue of there being one price for a large number of predictions. Interesting things happen from this principle:1 in our case, that cyclical stocks can trade at what appear to be low multiples in times of rapid growth.

I. A cyclical run-up is not necessarily a bubble

Cyclicality is a double edged sword: rapidly increasing demand for an asset-heavy good pushes prices up because it takes a while for supply to catch up → competitive intensity chases high growth, incumbents chase the new demand with large capital outlays → a combination of new supply and/or a decrease in demand crushes prices, with a levered effect on margins.

The length of a capital cycle partly depends on the rationality of industry players. Irrational behavior happens when incumbents aggressively pursue capacity expansion with no clear view on how long the demand surge will last. Rationality, more often found in oligopolies due to their high barriers to entry, is cautious supply expansion where demand is visible for long enough to earn high through-cycle returns on invested capital.

Investors know all about this, so when they see a cyclical industry in the middle of a demand surge, they know better than to act as if that is the new normal. But even if they try to be careful, the lag in information digestion leads to high share price volatility. Each new data point that confirms the cycle has legs justifies an upward adjustment to mid-cycle earnings.

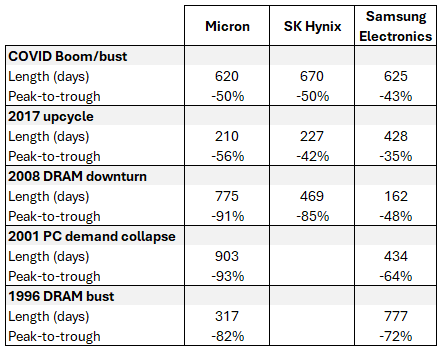

The reverse is true, too. An embattled company in the midst of a 300-day long drawdown competes for investors’ attention with more exciting parts of the economy, and might earn returns below its cost of capital for an unknown amount of time before the cycle turns. If the pain is particularly dreadful, the industry might go through waves of consolidation. Indeed, our Memory Three represent >95% of worldwide memory sales today, up from ~60% in 2008.

It’s impossible to accurately predict when cycles start or end, and most importantly their magnitude. Crucially, a sharp increase in share price for a cyclical company does not mean you should stay away or, worse, constantly “call the top”. New information, feedback loops between demand and supply, technological advances, competitive intensity, decision-making rationality, the minimum viable size of a capital outlay to meet a portion of demand, etc. all play their role in changing what reality looks like from one day to the next.

A perfect example of this is AMD CEO Lisa Su doubling her expectations for the size of the server CPU market by 2030, between November 2025 and May 2026. There’s no question about the cyclicality of the CPU industry, but had you accepted the November figure in your analysis and buried your head in the sand, you likely would have felt the subsequent >75% share price gain as utterly irrational. If you accept her new figure today, the run-up is reassessed entirely.

II. Memory is still priced as cyclical today

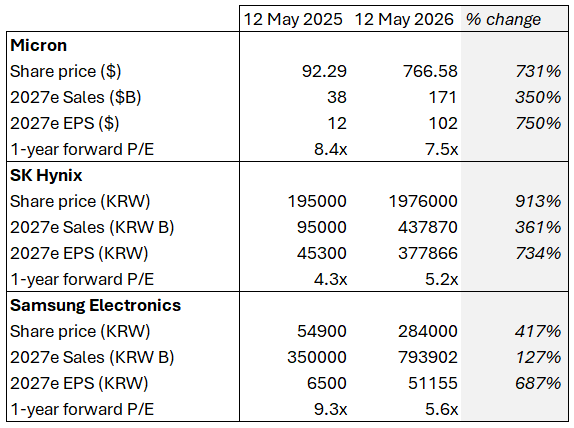

A quick look at the forward price to earnings ratio for the Memory Three shows that the weighing machine is still firmly in the camp of cyclicality.

If 2027 expectations were held constant and investors adjusted only their belief about cyclicality, you could reasonably imagine a world where the share price of the Memory Three has a lot more room to grow through multiple expansion. In reality, investors hold a number of expectations at once, most of which have an impact on others, such that the incredible surge in EPS expectations is at the center of why the multiples seem so “low”.

The large capital expenditures needed to bring these numbers to life are only partially visible on the EPS line in the form of depreciation. Micron will spend upwards of $25B in capex in 2026 (23% of 2026e sales), and probably more than $35B2 in 2027 (23% of 2027e sales). SK Hynix will spend as much as $60B in the next two years, and Samsung above $73B in 2026 alone3.

Taking Micron as a pure-play example, the useful lives for its property, plant and equipment are “of generally 10 to 30 years for buildings, 7 years for production equipment, [and] up to 7 years for other equipment”. When the cycle turns, the level of mid-cycle earnings will be heavily impacted by the straight-line depreciation it accumulated in the run-up. Whether the company’s capex figures make sense with today’s information is up to you, but long-term returns will depend on whether they make sense with the next five years in the rear view mirror.

III. Look for confirmation, then act

I agree with Michael Burry’s assessment that parabolic rises are a good signal to reduce positions, and not necessarily a good moment to short. Two reasons why I believe this: (1) the length and magnitude of capital cycles are unknown, and (2) a parabolic share price increase can only make sense as long as reality proves the thesis that supports it.

Instead of trying to time a reversal from the wrong side, you should use the cycle’s long-term nature to your advantage by mapping what needs to happen for the memory trade to die. By waiting for confirmation that we’re over the hump, you will incur a sharp drawdown (or miss it, if you are short). Long-term expectations of hyperscaler capex have surprised upward for three years now, and the feeling of this being the “new normal” supports lofty valuations at the sector and index level. At the first sign of trouble, such as when Deepseek’s LLM burst onto the scene with claims it took only $6m to train, Nvidia’s share price fell by 17%. If it can happen to the most valuable monopoly on Earth, what do you think happens to our Memory Three if such disruption comes to light tomorrow?

But here’s the thing: when the cycle turns, the initial drawdown is a drop in the bucket compared with what’s to come.

IV. Understand it to kill it

Before you can figure out what can kill a thesis, you need to know why it exists in the first place.

The bulk of AI workload happens when models and agents think about what to do next, a process called inference.

During inference, the GPU sits idle waiting for memory to supply model weights and KV cache data fast enough. This memory bandwidth wall means GPUs are only as fast as memory is. High-bandwidth memory (HBM) scales the wall by sitting on the same interposer as the GPU die, delivering more bandwidth than traditional GDDR or DRAM could.

Skip this bullet if you don’t need to know more about why HBM is so important.

Today, GPUs actually spend more time moving weights and KV-cache than doing tensor math, because inference decode is extremely arithmetically intensive in multi-head latent attention architectures. HBM4 is fast, but it’s still going to be the bottleneck for token throughput in 2026 because every generated token requires streaming the entire model weights from HBM to the compute units, plus reading a growing KV cache.

Only three companies in the world make memory at the level of sophistication needed for modern data center GPUs: Samsung Electronics, SK Hynix and Micron. The latter two are pure-play memory companies, while Samsung Electronics also sells smartphones, TVs and display panels.

The Memory Three have limited supply, not just due to factory cost and scale but also due to yield and other technical constraints that can ruin a large portion of capacity.

Multiple years’ worth of supply is under contract and long-term agreements lock in volumes, allowing for strong pricing power at each renegotiation window.

As pricing increases with no equal increases in volume, operating leverage allows earning expansion far beyond sales growth on a percentage basis.

For as long as these conditions hold, the Memory Three will command earnings expectations that the market keeps undervaluing, because investors cannot see where the feedback loop ends.

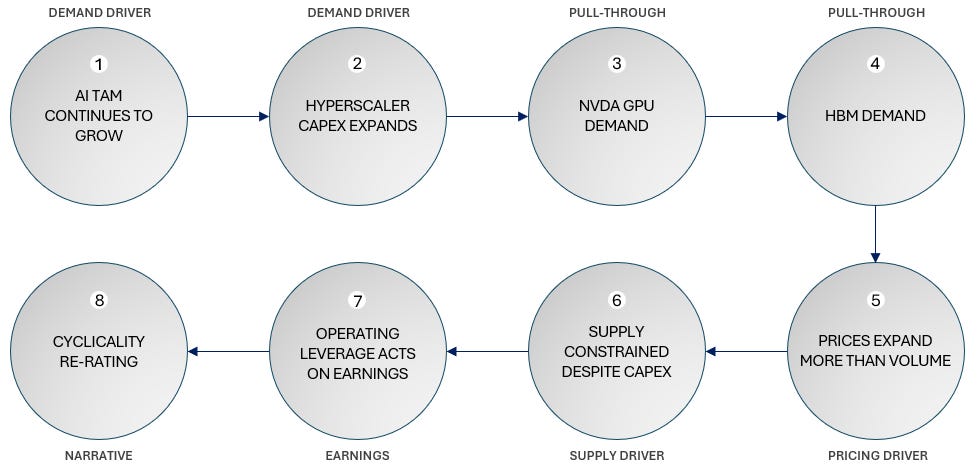

Now, let’s cleanly map out the narratives and fundamentals in a single line of causality:

Points 1, 2 and 3 are existential to the rally.

2: Hyperscaler Capex Expands

It is the lynchpin for the entire AI trade, not just memory, but it would indeed have drastic implications on the Memory Three. At its core, the AI rally exists because hyperscaler capex is expected to reach $650B in 2026, a figure that keeps surprising to the upside every quarter since the start of 2023. This seemingly never-ending race to the top, reaching ~2% of US GDP this year, leads to ramped up capex plans for the entire semiconductor industry in a bid to increase supply at numerous bottlenecks, from memory to niche glass cloth manufacturers.

The catalyst watch is really simple here: every quarter, you have to be ready for at least one of the hyperscalers to announce a capex target that falls short of the “beat & raise” dynamic we’ve become accustomed to. The result would be an immediate, sharp drawdown in all corners of the semiconductor industry, and you wouldn’t miss it.

Points 4 and 6 are where we find two catalysts where the memory trade itself loses steam without crumbling with the rest of the AI thesis.

4: HBM Demand

HBM demand is assumed to grow because GPUs are as fast as memory will allow. But this is only true insofar as Nvidia, Google (which is bringing TPUs to select customers in 2026) and AMD do not figure out how to get around this bottleneck that is clearly shifting the value capture of the AI rally away from the XPU designers. Manufacturing improvements isn’t even where I’d put the highest probability. For me, the larger risk is algorithmic improvements that shift the burden away from the problem that HBM solves. The catalyst would be the announcement of an algorithmic or manufacturing breakthrough targeting memory usage directly, ideally shifting the burden of speed away from it, or the announcement of a new LLM architecture that activates fewer parameters per token while keeping performance at the leading edge.

Note that the Memory Three tanked in late March when Google published TurboQuant, a compression algorithm that compressed KV cache by ~4-6x, but later rebounded as it became clear that such improvements would only boost inference working memory, not training memory or model weights. In a typical case of Jevons paradox, the technological improvement of better compression simply increases the addressable use cases for high performance memory. Thus, point four needs a catalyst that targets HBM memory as a hardware category, and for that to happen it needs to have a clear downward impact on future memory volumes. This is the only point where I think the catalyst could be a slow bleed rather than an overnight event. Inference efficiency compounds pretty rapidly, and it’s unclear to me at what point the memory-per-useful-compute ratio falls enough to eat into the cycle.

6: Supply Constrained Despite Capex

We sometimes assume capex announcements have a 1:1 ratio with HBM supply coming online, but HBM stacking has yield risk at every new generation. Samsung discovered this the hard way when HBM3E qualification for Nvidia was delayed by 18 months. For catalyst watch, ideally you’d look for fab qualification announcements in conjunction with shipment ramp data, the latter of which is more likely to be gauged by the language of memory executives on earnings calls than in press releases. At any rate, I’m not advocating for you to be first! If the yield-gate condition is triggered at any player, you can expect at least medium-term pain, because revenue expectations two years out tend to assume qualification goes smoothly.

You might think a qualification failure at one memory company might be nullified (in basket-trade market cap impact) by the commensurate increase in value at the other two. That’s only true if the other two (1) pass qualifications themselves and (2) have enough capacity to supply the void left behind by the disqualified.

There’s also the looming risk of ChangXin and YMTC, the Chinese competitors who will likely get up to HBM3 levels of manufacturing prowess by 2027, increasing supply materially enough beyond 2027-28 that the effect would be felt on price. It’s more of a long-term catalyst than a near-term one, but it’s worth keeping an eye on.

Finally, the sharp increase in expected earnings at SK Hynix and Samsung has spurred a top South Korean policymaker to say “the nation should pay citizens a “dividend” using taxes on AI profits”, but as this sort of policy doesn’t strictly impact prices and volumes, I don’t think it’s a meaningful catalyst today.

Parabolic price charts are scary, and it’s true they never continue forever. But that’s not enough to justify a short at any time, or even to reduce your positions if you’re not seeing anything disprove the thesis that led you to invest in the first place. The run-up in share price for the Memory Three seems mostly justified by future expectations as they stand today. The market still believes they are cyclical, but keeps being surprised by incoming data on just how much demand there is for memory.

I think the way to play around the increasing importance of memory stocks in global portfolios is to know what kills the thesis, and to take profit (or enter into a short position, although that’s materially riskier) only when your confidence is high that we’re on the other side of the cycle. You should treat the almost unavoidable initial drawdown as a cost for increasing your certainty past its “call to action threshold”.

For example, the high share price volatility of distressed companies stems from the fact that equity claims act like a call option on enterprise value. At or near the strike, the value of equity varies immensely based on new information.

This includes non-memory related spend, but we can assume Samsung’s memory related capex is in the same ballpark as its two competitors.

Disclosure and disclaimer.